A Three-part series written by Thomas E. Lah, Executive Director, TSIA

Data-Driven Insight

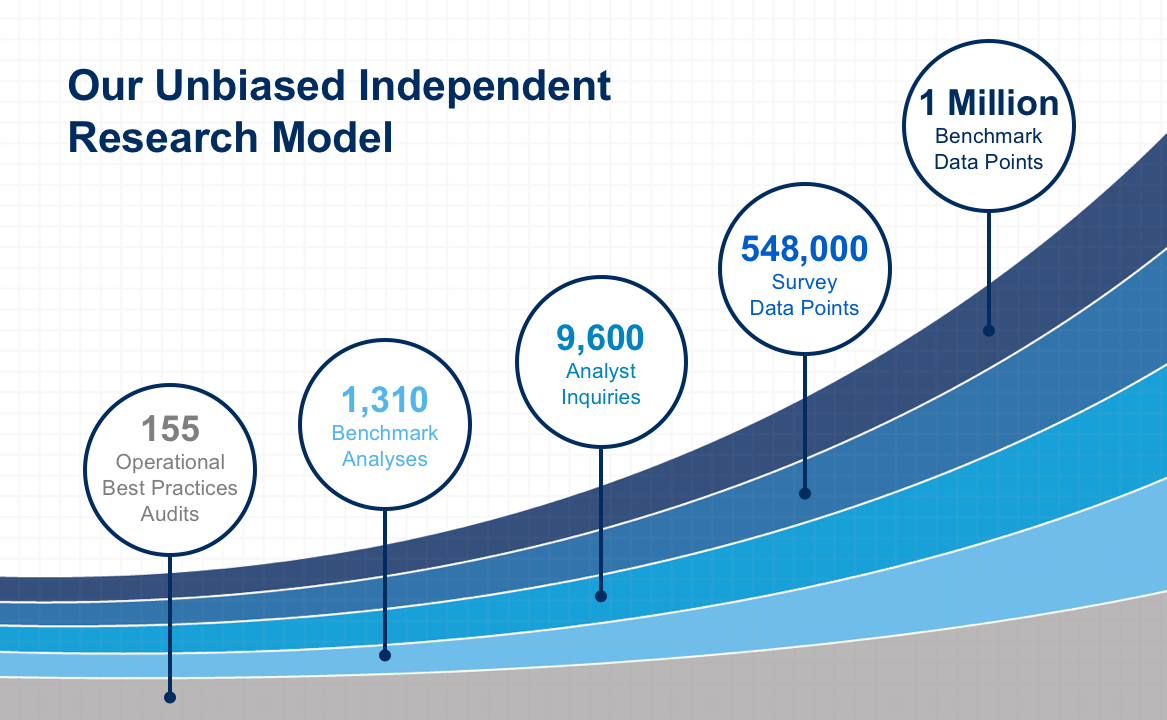

Before I tell you things you may not believe, I first need to explain why I am credible to make these statements. I serve as the Executive Director of the Technology Services Industry Association (TSIA). TSIA is a research hub for the technology industry. Member companies come together to collaborate on the toughest challenges facing technology solution providers. In 2017, TSIA will publish over one hundred unique research deliverables and conduct over twenty industry studies, covering everything from customer success funding models to the profitability performance of complex managed service contracts. Figure 1 summarizes the volume of data we leverage to analyze the economics of the technology industry.

Hitting a Wall

Now, sitting on top of all that data, what if I made the following statement:

“Selling technology is becoming a low growth, low margin endeavor.”

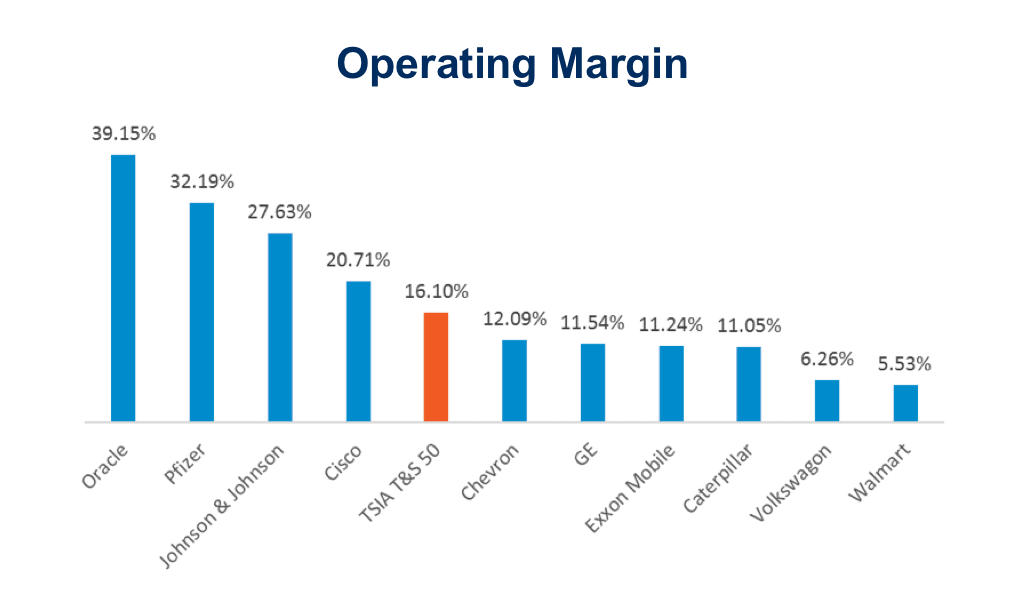

Would you believe me? I mean, isn’t the technology industry all about high growth, high margin business models? Historically, yes. Companies selling complex hardware and software have enjoyed some of the highest growth and highest margin business models in the history of business models. For the past decade, TSIA has been tracking the performance of fifty of the largest tech companies on the planet. In 2014, the average operating margin of those companies was over 16%. In that same year, Oracle software was generating almost 40% in operating margin!

But those beautiful business models are under pressure. In 2013, TSIA published a book titled B4B: How Technology and Big Data Are Reinventing the Customer-Supplier Relationship.[i] The book predicted an incredible disruption to technology industry business models. Why? Our data was showing that technology providers were beginning to grapple with the following realities:

- Commoditization of feature functionality: Customers are less willing to pay a premium price for technical capabilities. They are much more interested in value realization from technology solutions. This trend is putting downward pricing pressure on both hardware and software offerings.

- Acceleration of new consumption models: Customers continue to explore new models for purchasing technology capabilities. Technology-as-a-service (XaaS) and managed service offerings continue to see double digit revenue growth while traditional hardware and software license revenues contract or remain flat.

- Financial models are shifting: The revenue mix of technology providers continues to shift. Less revenue and margin from selling technology as an asset. More revenue from services and subscriptions. This is forcing CFOs to rethink overarching financial models—a thought exercise many companies loathe to conduct.

- New offer types: The tried-and-true service portfolios are losing their enamor with customers. Traditional support, education, and professional service offerings are designed to implement technology and keep it running. Customers want help optimizing their use of technology. This drives the demand for new classes of services such as adoption services (help the customer move from low to effective adoption of your technology), managed services (help the customer optimize ongoing operational costs), and outcome services (help the customer achieve specific business outcomes).

- New organizational capabilities: Finally, all of the above trends are forcing technology companies to establish new organizational capabilities. New employee skills, new business processes, and new performance metrics that align with changing customer demands and reengineered financial models.

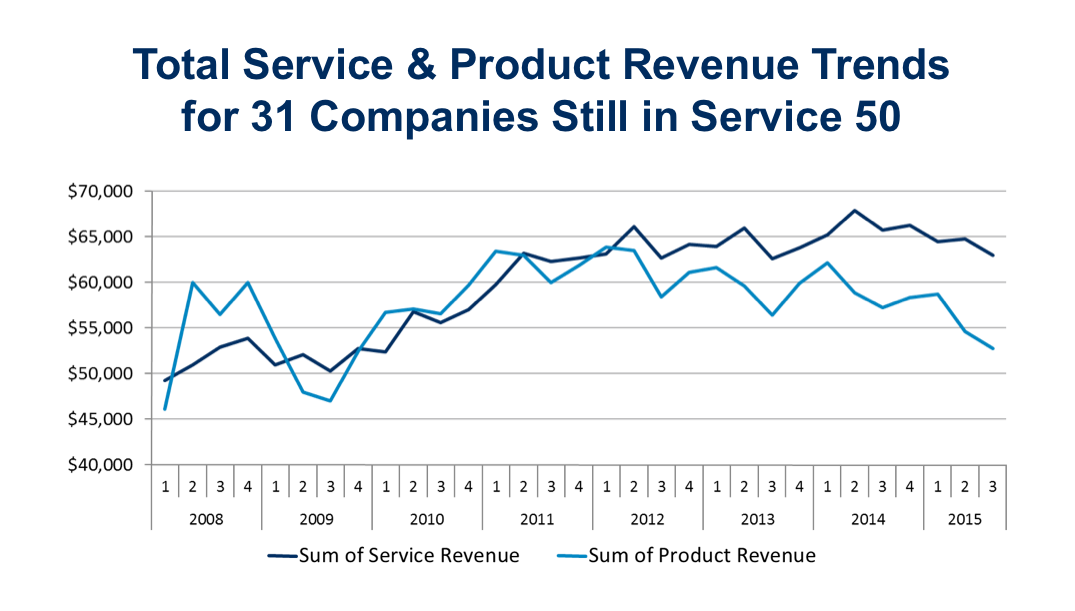

By 2017, the impact of these trends was evidenced for all to see. For many of the well-established tech companies, product revenues plummeted at double digit rates. Traditional service revenues (support, education, field services) also waned as tracked in the Technology & Services 50 Index.

Figure 1: Product and Service Revenue Trends

[i] Wood, J.B., Todd Hewlin, and Thomas Lah. 2013. B4B: How Technology and Big Data Are Reinventing the Customer-Supplier Relationship. San Diego: Point B, Inc.

Where are the product revenues going? Some of them are simply evaporating, as customers pay less for the same or more technical capacity. Other product revenues are being converted to service revenues as customers chose to rent technology as opposed to own technology assets. That second trend is pummeling the tech business models. Welcome to the subscription economy.

Impact of the Subscription Economy

When customers decide to rent and not own assets, three things happen:

- Customers do not pay for capacity they do not need.

- Customers are not stuck with assets they no longer want or need.

- Customers have more flexibility to switch providers.

These three realities break down the traditional tech business model, where customers made significant up front investments to purchase assets. Once these investments were made, the customer then paid ongoing maintenance costs as an insurance policy to protect the value of those tech assets. In the subscription economy, the technology provider is responsible for maintaining the assets. No high margin insurance policy required.

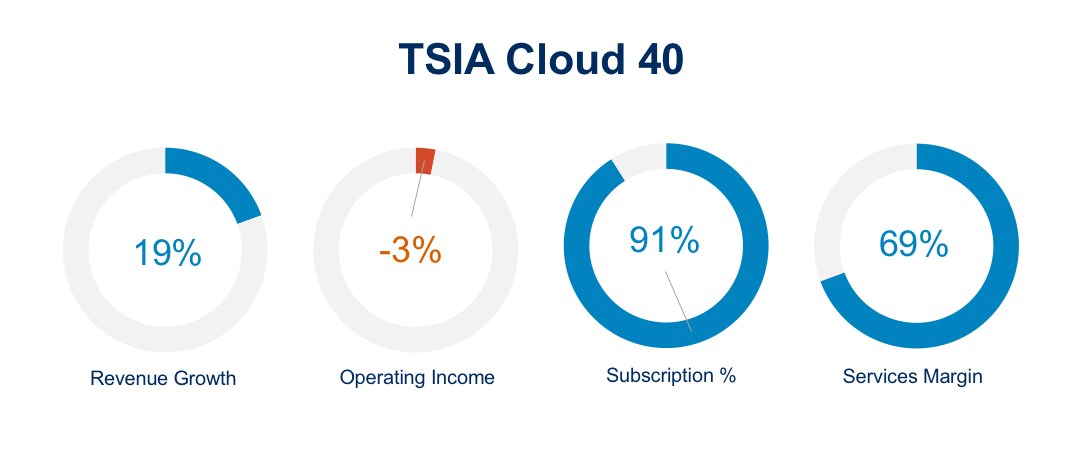

In theory, subscription business models can result in a high margin business where tons of customers are paying year after year to access a common platform. At TSIA, we believe the potential is there. However, the vast majority of tech companies are not optimized to support subscription business models. Even the born in the cloud companies! We track forty of the largest cloud computing companies on the planet. Their revenues are growing at double digit rates, but, on average, these companies are losing money.

What Saves Tech?

A common question we receive at TSIA today:

“How can a technology company drive profitable growth?”

Traditional tech business models are highly profitable, but not growing. Subscription tech business models are growing fast but not yet proving very profitable. Our response to this question is simple:

Embrace as-a-service offers (this is where the revenue is going) that are anchored on business outcomes (not feature functionality, which is commoditizing) and supported by a customer engagement model that cost-effectively drives the adoption, expansion, and renewal of your offers (this is where most tech companies are failing).

The answer is simple, but the execution is wicked hard. In the next article, I will discuss what it means to embrace as-a-service offers in a tech business model.

[1] J.B. Wood, Todd Hewlin, and Thomas Lah. 2013. B4B: How Technology and Big Data Are Reinventing the Customer-Supplier Relationship. San Diego: Point B, Inc.